What is a Home Inventory? A home inventory is a detailed record of everything you have inside your home. It includes information

such as the purchase price, purchase date, and description of each item. Creating a home inventory is essential for insurance purposes as it helps determine the value of your belongings and ensures that you have adequate coverage in the event of theft, damage, or loss due to a natural disaster. It is important to regularly update and maintain your home inventory to include any new purchases or changes in value. There are various methods to create a home inventory, including using inventory apps, spreadsheets, or simply writing it down on paper. Regardless of the method you choose, the key is to be thorough and include as much detail as possible for each item.

Why Should I make a Home Inventory? Benefits of Having an Up-to-Date Home Inventory

A home inventory is a comprehensive list of all your personal belongings and valuables within your home. While it may seem like a daunting task, creating and maintaining an up-to-date home inventory can offer a range of benefits that make it well worth the effort.

One of the main advantages of having a home inventory is that it can help ensure you have sufficient insurance coverage. By accurately documenting all your possessions, you can easily determine the value of your personal property, which is crucial when purchasing homeowners or renters insurance. This can help you avoid being underinsured and facing financial loss in the event of a natural disaster or other unforeseen circumstances.

In addition, having a detailed home inventory can expedite the claims process with your insurance company. Instead of relying solely on memory to recall what items were lost or damaged, you can provide your insurer with an organized record of your belongings, including purchase prices, descriptions, and even photos or videos. This can greatly streamline the claims process and assist in receiving fair compensation for your losses.

Furthermore, an up-to-date home inventory can be beneficial when it comes to tax deductions. If you experience a loss due to a theft or natural disaster, you may be eligible to claim a casualty loss deduction on your taxes. Having a thorough inventory, complete with purchase receipts and other supporting documentation, can make it easier to calculate and substantiate your losses for tax purposes.

To make the process even more convenient, there are several inventory apps available that can help you create and store your home inventory digitally. These apps often allow you to input item details, attach photos, and even record videos of your belongings. Alternatively, you can use your smartphone to create a detailed video inventory that captures each room and its contents. Whichever method you choose, it is important to regularly update your inventory to reflect any new purchases or changes to your possessions.

When it comes to storage, consider keeping your home inventory in a safe and easily accessible location. Cloud storage is a popular option as it allows you to access your inventory from anywhere and ensures it is protected in the event of physical damage to your home. Alternatively, you could store a physical copy of your inventory with a trusted person, such as a family member or your insurance agent.

In conclusion, creating and maintaining an up-to-date home inventory can provide numerous benefits. From helping to ensure sufficient insurance coverage to expediting claims processing and facilitating tax deductions, a home inventory is a valuable tool for protecting your personal belongings. Whether you choose to use an inventory app or create a video inventory, remember to regularly update your inventory to keep it accurate and reliable.

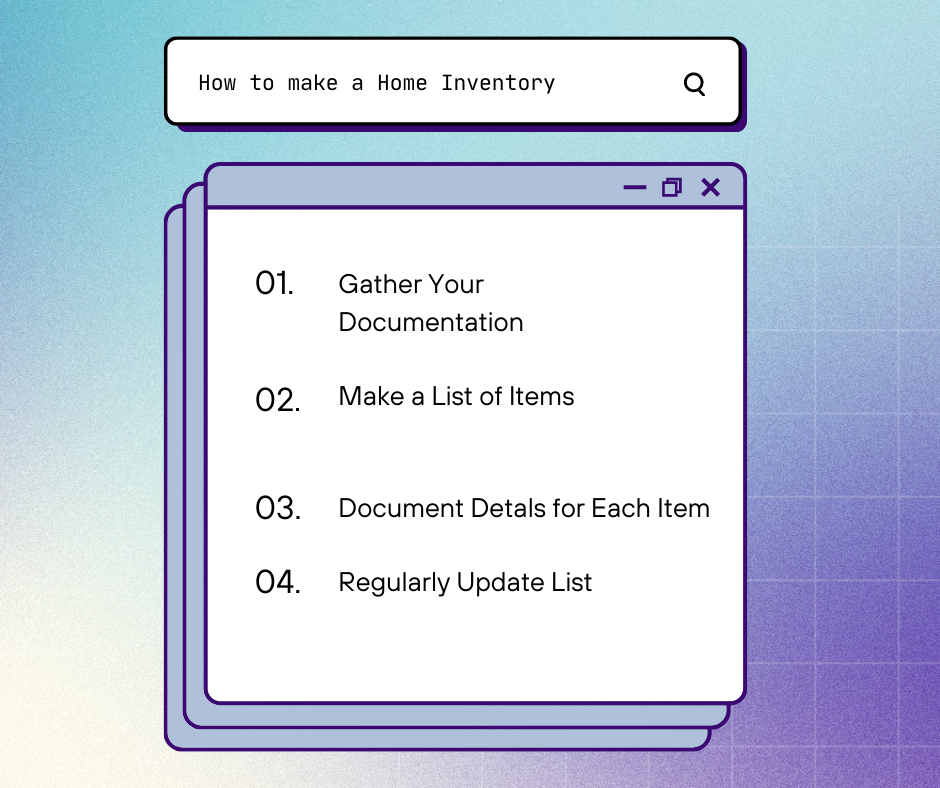

Gather your Documentation Documentation Needed

Step 1: Gather your Documentation

Creating a comprehensive home inventory for insurance purposes starts with gathering the necessary documentation. This includes sales receipts, photographs or videos, and digital copies of important documents.

Sales receipts serve as proof of purchase and are essential when determining the value of your possessions. Be sure to collect and organize receipts for major items such as electronics, furniture, and appliances. These receipts provide valuable information such as purchase prices, brand names, and model numbers, which are crucial for accurately assessing your personal property coverage.

Photographs or videos are also vital for documenting your belongings. Take clear, detailed photos or videos of each item, capturing multiple angles and any distinguishing features. This visual evidence helps both you and your insurance company accurately identify and verify the condition of your possessions in the event of a claim.

Additionally, create digital copies of important documents related to your possessions. This may include warranties, appraisals, and any certificates of authenticity for high-value items like jewelry or artwork. Storing these documents digitally ensures they are easily accessible and protected from physical damage or loss.

By gathering and organizing your sales receipts, photographs or videos, and digital copies of important documents, you are taking the necessary steps to create a comprehensive and reliable home inventory for insurance purposes. This documentation will play a vital role in accurately valuing your personal property and expediting the claims process in the event of a loss.

Sales receipts

When creating a home inventory for insurance purposes, keeping sales receipts for expensive items is of utmost importance. These receipts play a vital role in documenting the value and authenticity of your possessions, providing several benefits throughout the claims process.

Firstly, sales receipts serve as solid proof of purchase. Insurance companies require evidence of ownership and purchase prices to accurately assess the value of your belongings. By having sales receipts readily available, you can easily provide this information and avoid any disputes regarding the value of your items.

Moreover, sales receipts act as additional evidence during the claims process. In the unfortunate event of a loss or damage to your expensive items, having sales receipts can help validate your claim and streamline the process. Insurance companies often request proof of ownership and the purchase price of damaged or stolen items. Sales receipts provide tangible proof, making it easier for the insurance company to evaluate your claim and process your reimbursement quickly.

In summary, keeping sales receipts for expensive items when creating a home inventory for insurance purposes offers significant benefits. These receipts provide concrete evidence of purchase, which accurately reflects the value of your possessions. Furthermore, they serve as critical evidence during the claims process, making it more straightforward and seamless for both you and your insurance company.

Photographs or Videos

Creating a comprehensive and detailed inventory of your personal belongings is crucial for insurance purposes. One effective way to do this is by using photographs or videos to create a digital home inventory list. Here are the steps to follow:

1. Use a smartphone: To ensure clear and high-quality images, it is recommended to use a smartphone with a good camera.

2. Take clear shots of each item: Start by taking photographs or videos of each item individually. Capture multiple angles and close-ups to provide a clear visual record. Don't forget to zoom in on any identifying features or serial numbers.

3. Photograph or video entire rooms: Move from room to room, capturing shots of the entire space. Include the walls, ceilings, and floors. This will help provide context and document the overall condition of your home.

4. Focus on specific areas: Pay attention to specific areas like drawers, closets, and cabinets. Open them and capture the contents. This will help you remember what you have stored in these spaces.

5. Document individual items: For valuable or high-value items, take extra care to capture their details, such as brand, model number, and any unique features. This will be helpful in evaluating their worth and authenticity.

It's important to create your home inventory list using the photographs or videos as soon as possible. Organize them by room or category, and include important details like purchase prices, dates, and any additional information that may be relevant. By having a digital home inventory, you can easily share it with your insurance company in the event of a claim, making the process smoother and more efficient.

Digital Copies of Important Documents

Digital Copies of Important Documents

In addition to photographing or recording your personal belongings, it is also important to create digital copies of important documents for insurance purposes. This includes documents such as sales receipts, appraisals, and warranties for valuable items. By having digital copies, you can easily access and provide proof of ownership in the event of a claim. To create digital copies, you can use a scanner or simply take clear photographs of each document. Make sure the text and details are legible, and organize them in a folder on your computer or cloud storage. It is also a good idea to keep copies of these documents in a secure location outside of your home, such as a safe deposit box. Creating digital copies of important documents will provide an added layer of protection and peace of mind in the event of a loss or damage to your personal property.

Step 2: Make a List of Items

When creating a home inventory for insurance purposes, it is important to include a comprehensive list of the items in your home. This will help ensure that you are properly covered in the event of a loss or damage.

Here are the types of items that should be included in your home inventory:

1. Valuable items: This includes any items of significant value, such as jewelry, artwork, antiques, or collectibles. Be sure to include detailed descriptions and, if possible, photographs or appraisals.

2. Expensive individual items: Take note of any high-value items that you own, such as electronics, appliances, or furniture. Include the make, model, and purchase price of each item.

3. Electronic equipment and appliances: This category includes items like computers, laptops, televisions, cameras, and kitchen appliances. Take note of any serial or identification numbers for these items.

4. Furnishings: Don't forget to include your household furnishings, such as sofas, beds, dining tables, and chairs. Include a description of each item, including the brand and any distinguishing features.

By including these types of items in your home inventory, you can ensure that you have adequate coverage for your personal belongings. Remember to update your inventory regularly and keep it in a safe place, such as a digital inventory app or a physical inventory document.

Valuable Items

When creating a home inventory for insurance purposes, it's crucial to identify and record any valuable items separately in your list. These are high-value items that may require additional coverage on your homeowners insurance policy. Examples of valuable items include jewelry, fur, rare keepsakes, and certain electronics that exceed a certain threshold, such as $1,000 to $2,000.

By documenting these valuable items, you ensure that they are properly accounted for in case of loss or damage. Include a detailed description of each item, including any distinguishing features, and if possible, take photographs or provide appraisals to support their value. This separate section in your home inventory list will make it easier for your insurance company to assess the worth of these items and provide appropriate coverage.

Remember, valuable items are often subject to a coverage limit on standard homeowners insurance policies. If your valuable items exceed this limit, consider purchasing additional coverage to safeguard their full value. By including these valuable items in your home inventory, you'll have a comprehensive record of your personal belongings and valuable possessions, providing you with peace of mind in the event of a loss or natural disaster.

Expensive Individual Items

Expensive Individual Items:

1. Identify and list high-value items: Start by identifying any expensive individual items in your home, such as jewelry, artwork, or collectibles. Make a separate section in your home inventory list specifically for these items.

2. Provide detailed descriptions: For each expensive item, include a detailed description, including any distinguishing features, such as brand, model, or unique characteristics. This will help your insurance company accurately assess their value.

3. Record purchase prices and appraisals: Include the purchase price of each expensive item in your inventory. If you have appraisals for these items, attach them or include copies in your inventory. Appraisals provide proof of an item's value and can assist in the claims process.

4. Determine replacement cost: Research and determine the current replacement cost of each expensive item. This is the amount it would cost to replace the item with a similar one in today's market. The replacement cost is essential for ensuring you have adequate insurance coverage for these items.

5. Evaluate insurance coverage: Review your homeowners or renters insurance policy to determine if it provides sufficient coverage for your expensive items. Often, standard policies have coverage limits for high-value items. If the coverage limit is inadequate, consider purchasing additional coverage, such as a floater policy, to fully protect your valuable possessions.

6. Keep digital copies: Take photographs or create video recordings of your expensive items and store them securely, either on a cloud-based platform or on an external hard drive. Digital copies serve as additional evidence of ownership and condition in the event of a claim.

By following these steps and ensuring you have adequate insurance coverage, you can have peace of mind knowing that your expensive individual items are properly protected.

Electronic Equipment and Appliances

Electronic Equipment and Appliances

In today's digital age, electronic equipment and appliances play a significant role in our everyday lives. From laptops and smartphones to kitchen appliances and televisions, these items are not only essential but often quite expensive. When creating a home inventory for insurance purposes, it is crucial to include these valuable electronics. Start by identifying any high-value electronic items in your home, such as computers, cameras, or home entertainment systems. Provide detailed descriptions for each item, including the brand, model, and any unique features. Be sure to record the purchase prices and keep receipts or invoices as proof of value. It is also helpful to research and determine the current replacement cost of each electronic item, as this will enable you to assess whether your insurance coverage is adequate. Consider taking photographs or creating video recordings of your electronic equipment and appliances to serve as additional evidence in the event of a claim. By including electronic equipment and appliances in your home inventory, you can ensure that you have the appropriate coverage to protect these valuable possessions.

Step 3: Document Details for Each Item Additional Details to Include on Your List

Document Details for Each Item

When creating your home inventory for insurance purposes, it is important to document the details of each item accurately. This will help ensure that you receive proper compensation in the event of a claim. Here are some additional details to include on your list:

1. Purchase Prices: Note down the purchase prices of your belongings. This will help determine their value at the time of loss or damage.

2. Actual Cash Value (ACV) or Replacement Cost Value (RCV): Specify whether you want to calculate the value of your items based on ACV or RCV. ACV takes into account depreciation, while RCV covers the cost of replacing the item at today's prices.

3. Model, Serial, and/or Manufacturer Number: If applicable, record the model, serial, and/or manufacturer number of each item. This information can be helpful in identifying the specific details of your belongings, especially for electronic equipment or valuable collectibles.

Remember to update your home inventory regularly. As you make new purchases or dispose of items, ensure that your list remains up-to-date. This will ensure that you have an accurate record of your personal belongings and will simplify the claims process in the future.

By including purchase prices, ACV or RCV values, and model/serial/manufacturer numbers on your inventory list, you can provide your insurance company with the necessary information to evaluate your coverage and ensure that you receive the appropriate compensation in the event of a claim.

Purchase Prices

When creating your home inventory list for insurance purposes, one crucial detail to include is the purchase prices of your belongings. These purchase prices are essential for determining the value of your items and calculating the appropriate insurance coverage.

Including purchase prices on your home inventory list helps establish the worth of your personal belongings at the time of loss or damage. Insurance companies typically consider the value of your items based on their purchase price, so having this information readily available ensures that you receive proper compensation in the event of a claim.

Keeping accurate and up-to-date purchase prices is crucial for maintaining the accuracy of your home inventory list. As you make new purchases or dispose of items, it's important to update the purchase price for each item on your list. This ensures that your insurance coverage accurately reflects the value of your personal belongings. Regularly reviewing and updating purchase prices helps you avoid any potential discrepancies or disputes with the insurance company during the claims process.

In conclusion, including purchase prices on your home inventory list is essential for determining the value of your items and calculating appropriate insurance coverage. By keeping accurate and up-to-date purchase prices, you can ensure that you are properly compensated for your personal belongings in the event of a claim.

Actual Cash Value (ACV) or Replacement Cost Value (RCV) of Each Item

Determining the Actual Cash Value (ACV) or Replacement Cost Value (RCV) for each item in your home inventory is of utmost importance for insurance purposes. ACV refers to the value of an item taking into account its depreciation over time, while RCV reflects the cost of replacing the item at its current market value.

Knowing the ACV or RCV of your personal belongings is crucial in ensuring that you have the right insurance coverage and will be adequately compensated in the event of a claim. Insurance companies typically base their payouts on ACV, so having an accurate and up-to-date home inventory list with the ACV of each item helps establish the worth of your possessions at the time of loss or damage.

However, some insurance policies offer the option of additional coverage for replacement cost, which covers the cost of replacing an item without considering depreciation. If you have this coverage, it is important to determine the RCV of your items so that you can fully utilize this benefit.

To determine the ACV or RCV of each item, consider factors such as the item's age, condition, and fair market value. You may need to consult professionals or online resources to determine the current value of certain items. Be sure to update your home inventory list regularly to reflect any changes in the value of your belongings.

By accurately determining the ACV or RCV of each item in your home inventory, you can ensure that your insurance coverage adequately reflects the value of your possessions, giving you peace of mind in the event of a claim.

Model, Serial and/or Manufacturer Number for Each Item (if Applicable)

Step 4: Update Your Inventory Regularly Reasons to Update Your Home Inventory Regularly

Topics: Insurance Claim, Home Inventory, Inventory Process, Edmond Home Insurance, Newcastle Home Insurance, Blanchard Home Insurance, Tuttle Home Insurance, Piedmont Home Insurance, Edmond Insurance Agency